Corporate & Large Entities

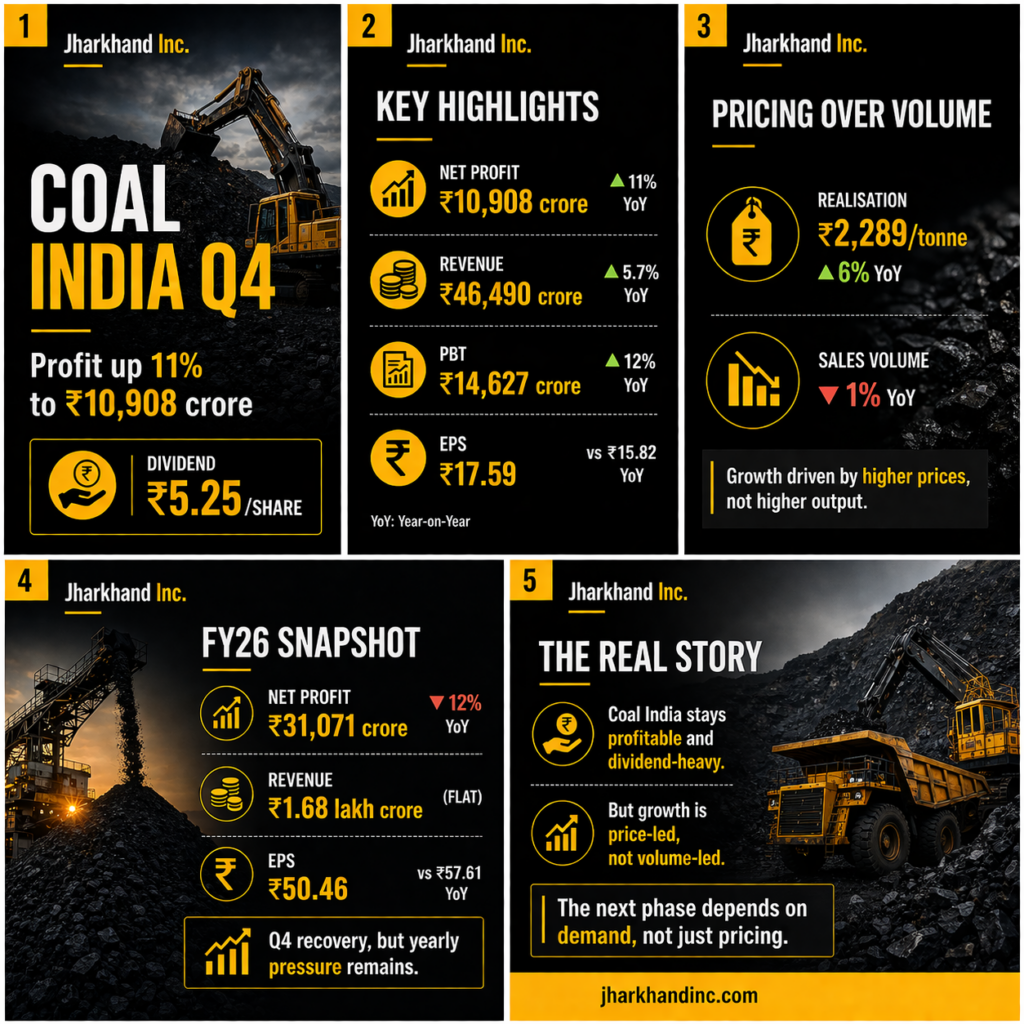

Coal India Q4: Profit Up 11%

Coal India reports an 11% YoY rise in Q4 FY26 profit to Rs 10,908 crore, announces Rs 5.25 dividend; growth driven by higher realisation despite flat volumes.

Coal India Q4 profit rises 11% to Rs 10,908 crore; board approves Rs 5.25 dividend

Coal India Ltd (CIL) reported an 11% year-on-year rise in consolidated net profit to Rs 10,908 crore for the March quarter, supported by higher realisations even as sales volumes remained largely flat.

The state-run miner had posted a profit of around Rs 9,740 crore in the year-ago period. Sequentially, net profit surged over 50% from Rs 7,157 crore in the December quarter.

Revenue growth modest; pricing offsets volume dip

Revenue from operations for Q4 FY26 stood at Rs 46,490 crore, up 5.7% YoY from Rs 43,962 crore.

- Average realisation rose 6% YoY to Rs 2,289 per tonne

- Offtake declined marginally by about 1%

The quarter’s performance was driven by pricing gains rather than volume expansion, reflecting stable demand but limited growth in dispatches.

Dividend maintained

The board recommended a final dividend of Rs 5.25 per share (face value Rs 10), reinforcing Coal India’s status as a high dividend-yield PSU.

The payout will be made through electronic modes in line with regulatory norms.

Margins steady; operating performance stable

- Profit Before Tax: Rs 14,627 crore (up 12% YoY)

- EPS: Rs 17.59 (vs Rs 15.82 YoY)

Margins remained stable despite cost pressures and provisioning adjustments.

FY26 performance under pressure

Despite a strong March quarter, full-year numbers indicate softness:

- Net profit: Rs 31,071 crore (down 12% YoY)

- Revenue: Rs 1,68,400 crore (flat to marginally lower)

- EPS: Rs 50.46 (vs Rs 57.61 YoY)

The divergence suggests that Q4 recovery has not fully offset earlier weakness.

Key accounting and structural factors

- Rs 1,458 crore provision for executive pay revision

- Stripping cost provision at Rs 56,504 crore

- Auditor issued unmodified opinion, with emphasis on accounting adjustments and governance aspects

Sector context

Coal India remains the world’s largest coal producer, central to India’s energy supply and public finances. The company contributes significantly through royalties, taxes and dividends, underlining its strategic importance.

Street view: pricing-led resilience

Coal India’s Q4 performance reflects a familiar trend:

- Stable demand environment

- Limited volume growth

- Earnings supported by better price realisation

The key monitorable going forward remains volume growth and demand visibility, especially amid energy transition pressures.

Bottom line

Coal India has delivered a strong quarter on profitability, but the underlying growth narrative remains price-driven rather than volume-led, keeping the medium-term outlook dependent on demand recovery and policy direction.

Ranchi turns vertical

Coal India Q4: Profit Up 11%